Special Depreciation Regime and new depreciation terms for certain assets are established.-

A) Through Legislative Decree No. 1488, published on May 10, 2020, establishes, exceptionally and temporarily, a special depreciation regime for taxpayers of the General Income Tax Regime, whose main aspects are as follows:

1. From the financial year 2021, buildings and constructions shall be depreciated by applying an annual rate of 20% until their total depreciation, provided that the following conditions are met:

(i) They are totally affected by the production of third category taxable income.

(ii) Construction began on January 1, 2020. For these purposes, the start of construction is understood as the moment when the building license or other document established by the Regulations is obtained.

(iii) Until December 31, 2022, the construction has an advance of the work of at least 80%. In the case of constructions that have not been completed until December 31, 2022, it is supposed that the progress of the work at that date is less than 80%, unless the taxpayer proves otherwise. It is understood that the construction has been completed when conformity of work or another document established by the Regulations has been obtained from the municipality.

The buildings and constructions included in this regime which start to depreciate in fiscal year 2020 apply the depreciation rate of 20% per year from fiscal year 2021, if applicable, except in the last fiscal year in which the rate of lower depreciation rate is applied.

This special depreciation regime may also be applied by taxpayers who, during the years 2020, 2021, and 2022, acquire ownership of buildings and constructions that meet the aforementioned conditions. This rule does not apply when said properties have been totally or partially built before January 1, 2020.

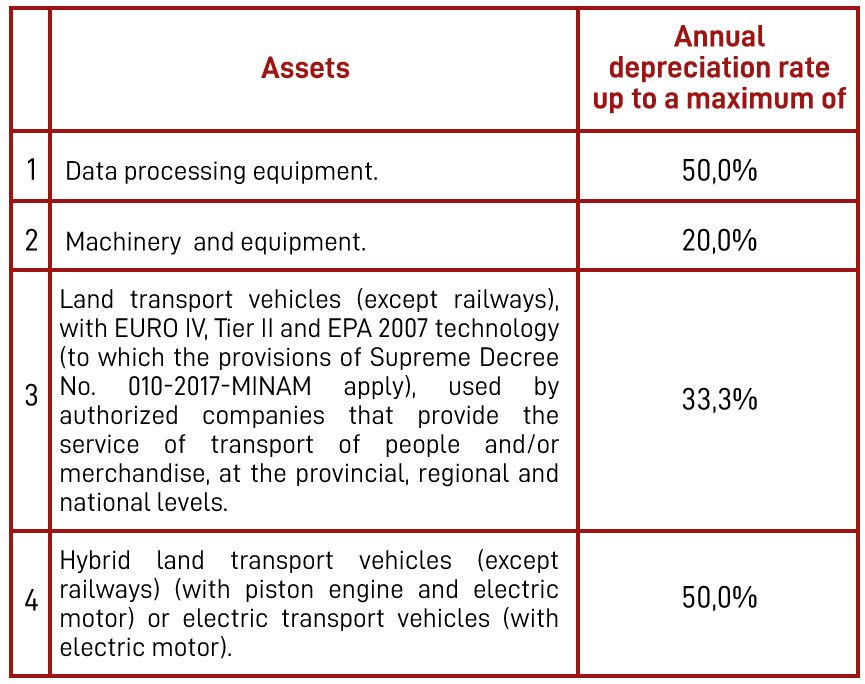

2. From fiscal year 2021, the assets listed below, acquired in fiscal years 2020 and 2021, assigned to the production of taxable income, shall be depreciated by applying the rate resulting from the following table, until they are fully depreciated:

B) Likewise, through Legislative Decree No. 1488, a special and temporary depreciation regime applicable to the fixed assets of taxpayers engaged in certain activities is established:

1. During the years 2021 and 2022, buildings and constructions with a depreciate value as at December 31 2020 shall be depreciated at a rate of 20% per year and, in those taxable years, are part of the fixed assets affected by the production of income from lodging establishments, travel and tourism agencies, or restaurants and related services, or fixed assets affected to the production of income from the performance of public non-sporting cultural shows. This rule applies with respect to buildings and constructions to which the special depreciation regime referred to in section A) above does not apply to them.

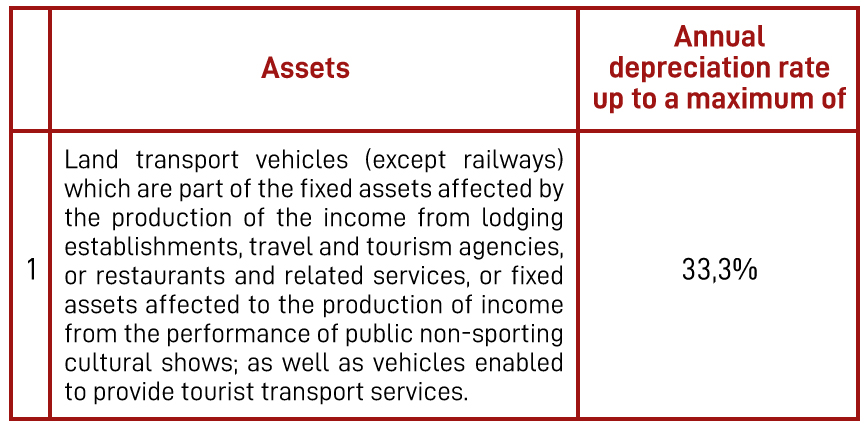

2. For the years 2021 and 2022, the assets indicated below with an impairment value as at December 31, 2020 shall be depreciated by applying the rate resulting from the following table.

C) The depreciation regimes provided for in Legislative Decree No. 1488 are not applicable to investments that, as of May 10, 2020, were included in the legal stability agreements signed under Legislative Decrees No. 662 and 757 and in other contracts signed with tax stability clauses, even when the stability period has not started to said investments; except for the waiver to said agreements or contracts.

D) Legislative Decree No. 1488 enters into force on January 1, 2021. A new Deferral and/or Fractionation Regime of tax debts administered by SUNAT (RAF).- Through Legislative Decree No. 1487, published on May 10, 2020, the RAF is created to provide payment facilities to taxpayers affected by the isolation and social immobilization measures ordered in the State of National Emergency.

1. In order to benefit from the RAF, taxpayers – among other requirements – must:

i. Have submitted the monthly IGV statements and interim payments from March and April 2020.

ii. When receiving third category income, have decreased the corresponding monthly income.For this purpose, as a general rule, the result of adding the monthly net income of the tax periods of March and April of the fiscal year 2020 with the monthly net income of the same periods of the fiscal year 2019 must be compared.

iii. On the business day prior to the submission of the application for placement, they must not have a balance greater than 5% of the UIT in any of the accounts held at Banco de la Nación for transactions subject to SPOT, nor income as collection to be charged against said amount.

iv. Have submitted all the statements corresponding to the tax debt for which the RAF is requested. When the debt is contained in a determination resolution, the statement shall not be necessary.

2. The tax debts that constitute income of the Public Treasury or ESSALUD, plus legal interests, may be accepted regardless of the state in which they are (including coercive collection or challenge).

In the case of payments on account of income tax, the following can be accepted:

i. The interest to be charged on income tax payments if the term for lodging the affidavit for the financial year and for payment of adjustment has expired, or if such affidavit has been filed, whichever occurs first.

ii. Interim payments for income of the third category for the periods January, February and March 2020, provided that the period of deferment and/or installment ends until December 31, 2020.

3. The debts generated by taxes withheld or collected are not included; those included in a bankruptcy proceedings or judicial or extrajudicial liquidation proceedings; nor are the debts for interim payments of the Income Tax from April to December 2020.

4. The submission of the application for placement suspends the collection of the tax debt.

5. The maximum terms granted in the RAF are: (a) deferment only: up to 6 months; (b) deferment and fractionation: up to 6 months of deferment and up to 30 months of fractionation; and, (c) fractionation only: up to 36 months.

6. The applicable monthly interest rate shall be 0.40%.

7. Through Superintendence Resolution, SUNAT shall regulate the form and conditions to submit the application for fostering to the RAF. 8. Placement may be requested from the date of entry into force of the Superintendence Resolution referred to in the previous paragraph until August 31, 2020.

The Virtual Court Registry Office of SUNAT is approved.- Through Superintendence Resolution No. 077-2020/SUNAT, published on May 8, 2020, the “Virtual Court Registry Office of SUNAT” (MPV-SUNAT)platform is created, in order to facilitate the virtual submission of documents linked to certain procedures. The main characteristics of this platform are the following:

i) Steps to follow:

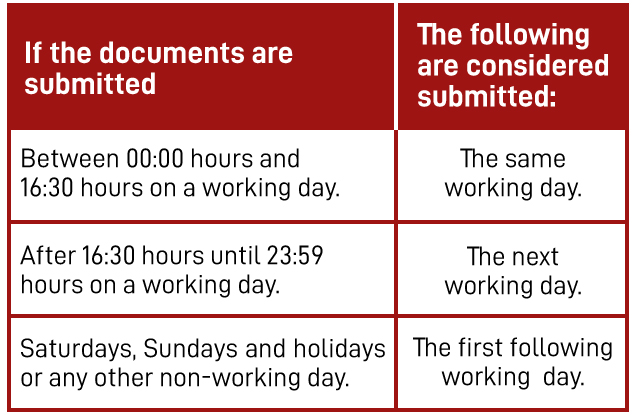

ii) Effects of the submission:

iii) Procedures under consideration: The Superintendence Resolution No. 077-2020/SUNAT does not specify the procedures that can be processed through the MPV-SUNAT. However, in the heading of the SUNAT website, a list of the procedures that would be included in this system has been published:

– Submission of claim and appeal resources (using the Summary Sheet).

– Refund requests using form No. 4949 (undue and/or excess payments, balance in favor of profit, early recovery of the VAT, definitive refund of the VAT, among others)

– Requests for material error, inscription to the RUC or communication of assignment of taxes, inscription in the Register of Entities Exempt from Income Tax, waiver of the exemption from the IGV and FORM 820 – VOUCHERS FOR UNUSUAL TRANSACTIONS.

– Process of cancellation in the RUC. – New issue of negotiable credit notes for loss, deterioration, partial or total destruction.

– Payment with valued documents.

– Statement of acceptance to the Law on the promotion of the agricultural sector and of the Law on the promotion and development of aquaculture (Form No. 4888).

iv) Impediments to work:

The MPV-SUNAT is not used for the submission of:

– Documents initiating automatic approval procedures, unless the relevant rule expressly states that the MPV-SUNAT shall be used.

– Statements, requests or other documents that according to the relevant rule may be submitted through the SUNAT Online Operations (SOL) system.

– Statements, requests or other documents to be made in person because this is established by law or supreme decree, because an application is required to validate information or because the nature of the documentation requires it (for example, letters of bail or notaries).

v) It is the taxpayer’s responsibility to constantly check the email provided, or, in the case of having SOL KEY, the electronic mailbox of SUNAT Operations Online.

vi) According to the communiqué shown in the MPV-SUNAT, the submission of documents through said system, exceptionally, shall not lead to the beginning of the processing period while the suspension of procedural deadlines declared in numeral 2 of the Second Final Supplementary Provision of the Emergency Decree No. 026-2020 and in article 28 of the Emergency Decree No. 029-2020.

Provisions related to the monthly affidavit of Income Tax and General Sales Tax (IGV).- Through Superintendence Resolution No. 076-2020/SUNAT, published on May 8, 2020:

i) The form “Declare Easy 621 IGV-Monthly Income” is amended so that third-rate Income Taxpayers can exercise the option to modify or suspend interim payments for the periods from April to July of 2020, in accordance with the special regime created by Legislative Decree No. 1471.

ii) Version 5.7 of PDT No. 621 IGV – Monthly Income is approved, which shall be used to submit the corresponding original, replacement or rectifying statements, except in the case where the option to modify or suspend interim payments is exercised from April to July 2020, in accordance with the special regime created by Legislative Decree No. 1471, in which case the “Declare Easy 621 IGV-Monthly Income” must be used. These new versions shall be available from May 11 at SUNAT Online Operations.

Registration and reactivation of the RUC through the Virtual Court Registry Office of SUNAT (MPV-SUNAT).- Through Superintendence Resolution No. 078-2020/SUNAT, published on May 9, 2020, the use is allowed of the MPV-SUNAT for the submission of the applications, forms and the necessary information for the registration in the RUC or the reactivation thereof. Two working days after the application is filed, SUNAT shall contact the taxpayer on the mobile phone number provided to validate the information and complete the procedure.