Requirements for the deduction of expenses for detriment are made more flexible.- Through Supreme Decree No. 86-2020-EF, from April 22, 2020, the requirements for the deduction of expenses for detriment from stocks are made more flexible:

i) The destruction to be carried out in the presence of the Notary Public or Justice of the Peace shall be communicated to SUNAT no less than 2 working days prior to the date on which the destruction shall take place. The regulation used to provide for a minimum period of six days.

ii) When the sum of the cost of stocks to be destroyed and the cost of stocks previously destroyed in the same period amounts to up to 10 UIT (S/.43,000), SUNAT shall accept that the destruction is supported in a report containing the information established in the Supreme Decree, the presence of a Notary or Justice of the Peace is not required, without prejudice to prior communication to SUNAT.

iii) The form and term in which the report is requested to be presented and the manner in which the prior communication to SUNAT shall be carried out shall be established through the superintendence resolution. As long as said resolution is not issued, the report shall be presented at the SUNAT offices within 5 workings days after the stock is destroyed and prior communication to SUNAT must be submitted to its office (except in the cases of destructions carried out until July 31, 2020 which have a special regulation and are mentioned below).

However, in view of the isolation measures issued by the government, certain transitional provisions have been established:

Amendments to the Indirect Disposal Regime of shares.- Supreme Decree No. 085-2020-EF has amended the Regulations of the IR Law in various aspects related to the “market value” of the shares (Peruvian and foreign) for the purposes of indirect disposal regime. Thus, this amendment affects the following aspects of the regime:

A. The market value of the shares to be considered for the purposes of the Tests: Pursuant to the amendment, the market value of the shares is considered, as the case may be:

i. The highest daily opening or closing price, in the case of listed shares.

ii. The value for discounted cash flow (new method), when the legal entity shows a foreseeable horizon of future flows or has elements such as licenses, authorizations or intangibles that allow the existence of such flows to be foreseen (and provided that what is indicated in section i. above is not applicable). The taxpayer must have a technical report to verify the valuation carried out under this method. This method was not included in the previous regulatory text.

iii. The equity participation value when they do not meet the conditions set forth in the Regulations for applying what is indicated in sections i. or ii. above, calculating on the basis of the last audited balance sheet of the issuing company, closed within 90 days prior to the disposal. Prior to the change introduced by Supreme Decree No. 085-2020-EF, this value was calculated on the basis of the last audited annual balance of the issuing company closed prior to the date of disposal.

If within 90 days prior to the indirect disposal of shares, a capital reduction is made in the non-domiciled legal person, the balance sheet to be considered shall be the one that corresponds before the aforementioned reduction, but within said period.

If the foregoing does not apply, the “equity value” shall be one of the following:

• The equity participation value increased by the monthly average market active rate in national currency (TAMN) published by the SBS. (provision introduced by the Supreme Decree).

• The appraisal value established within the 6 months prior to the date of the disposal or issue of shares or participations as a result of a capital increase.

B. How the 50% Test should be carried out: As appropriate, apply the valuation methods ii. or iii. aforementioned, the 50% Test must be carried out not only on the date of the disposal, but also in each of the 3 quarters preceding the one in which the disposal takes place (i.e. there are 4 quarters in total).

• For the 3 quarters prior to the disposal: the market value obtained by virtue of the balance sheets corresponding to the end of each quarter is used.

• For the quarter to which the disposal relates: the market value is determined according to the method that is applicable to the legal entity (i.e. discounted cash flow value or equity participation value). Prior to the amendment introduced by Supreme Decree No. 085-2020-EF, this analysis was done only once; that is, looking at the equity participation value according to the last audited annual balance of each company, closed prior to the disposal date.

C. Homogeneity of the methodology used for the preparation of the balance sheets: The balance sheets of domiciled and non-domiciled legal entities (on the basis of which the “market value” is determined) must be prepared based on uniform accounting policies. Otherwise, the balance sheet of the foreign entity must be reformulated according to the accounting policies applied to the Peruvian legal entity whose shares are indirectly disposed of. (Provision introduced by Supreme Decree No. 085-2020-EF).

D. Rules to determine the “tax base” (i.e. part of the income that shall be considered as “Peruvian source income” in case the transaction qualifies as “indirect disposal”): To determine the tax base, the rules provide that the value of market of the shares of the foreign entity vis à vis the market value of the shares of the Peruvian legal entity that are indirectly disposed of.

The change in this point relates to the “market value” of the shares of the entity from abroad, which must be considered for the purposes of calculating the tax base. The following provisions are incorporated:

• This value is expected to be the highest between: i) the transaction value; and, ii) the market value that is determined based on the applicable method as indicated in section A above (quotation, discounted cash flow or equity participation value). The previous Regulation did not provide for this comparison, referring only to the market value resulting from the listed value or equity participation value.

The market value determined in accordance with the foregoing is multiplied by the percentage of participation (i.e. equivalence percentage), determined in accordance with the provisions of the second paragraph of numeral 1 of subsection e) of article 10 of the Law, which is held at that date.

In the absence of an express provision that postpones its entry into force, the aforementioned changes must take effect from the day after the publication of Supreme Decree 085-2020-EF, that is, from April 22, 2020.

Amendments to the Special Regime of Early Recovery the General Sales Tax (IGV).- Through Legislative Decree No. 1463, published on April 17, 2020, the regime is extended until December 31, 2023 which consists in the return of the tax credit generated on imports and/or local purchases of new capital goods, by taxpayers whose annual net income is up to 300 UIT and who are covered by the MYPE Income Tax Regime or the General Income Tax Regime. This rule also provides that, exceptionally, IGV taxpayers whose annual net income ranges from 300 to 2,300 UIT, and which are covered by the MYPE Taxation or General Income Tax regimes regarding purchases of new capital goods made since January 1, 2020.

The deadline for issuing Digital Certificates and electronic payment vouchers is extended.- Through Legislative Decree No. 1370, SUNAT was authorized to act as a Registration or Verification Entity until June 30, 2020, for digital certificates requested by natural or legal persons generating annual net income of up to three hundred (300) UIT. This to enable taxpayers to obtain the digital certificates necessary for the issuance of electronic payment vouchers.Through Legislative Decree No. 1462, published on April 17, 2020, the stated period is extended until December 31, 2021.

Amendments to the Electronic Issuance System of payment vouchers.- Through Superintendence Resolution No. 073-2020/SUNAT, the following is provided:

i) Subjects who acquired the status of electronic issuer on April 1, 2020 by determination of SUNAT, because they chose to be electronic issuers in October 2019 (in the SEE-Taxpayer systems, SEE SUNAT Online Operations, SEE Biller SUNAT or SEE Electronic Services Operator) or because they were registered in the RUC in March 2020, may, exceptionally, issue payment vouchers in printed format until August 31, 2020. Invoices, payment forms, and credit and/or debit notes issued in printed format until August 31, 2020, shall not be required to contain the glosses “in contingency” and “required electronic issuer”.

ii) Subjects who acquired the status of electronic issuer by choice between November 2019 and February 2020, shall be considered as such, only from September 1, 2020. Therefore, they may continue to issue payment vouchers in format printed until August 31, 2020.

iii) Subjects who were registered in the RUC between February and May 2020, shall be considered as electronic issuers by determination of SUNAT, from September 1, 2020. Originally, said designation would have operated between May and August of 2020. This provision applies provided that, on the first calendar day of the third month following the month of their registration, these taxpayers have entered the MYPE Tax Regime or the Special Income Tax Regime or have entered the General Regime of said tax, on the occasion of the presentation of the monthly statement corresponding to the month of start of activities declared in the RUC; or, if no statement has been filed, they have communicated through the RUC, under the heading of taxes, that they opted for one of the aforementioned regimes.

iv) The appointment as electronic issuers of private pension fund administrators is postponed until February 1, 2021. Originally, said designation, established by article 2 of the Superintendence Resolution No. 318-2017/SUNAT, would start on July 1, 2020.

v) The designation as electronic issuers of the companies that provide the public telecommunications service and other supervised companies referred to in subsections b) to f) of paragraph 2.1 of the second final supplementary provision of the Superintendence Resolution No. 206-2019/SUNAT is postponed until October 1, 2020. Originally, its designation would operate from May 1, 2020.

Suspension of administrative deadlines is extended.- Through Supreme Decree No. 76-2020-PCM, published on April 28, 2020, the suspension of the calculation of deadlines for administrative procedures subject to positive and negative silence in process is extended, referred to in number 2 of the Second Final Supplementary Provision of the Emergency Decree No. 026-2020, for a period of fifteen (15) working days from April 29, 2020.

Place of presentation of statements prepared using the Telematics Statement Program (PDT) is modified.- Through Superintendence Resolution No. 074-2020/SUNAT, published on April 30, 2020, it is established that the presentation of the original statements, rectifications or substitutes that are prepared using the various PDTs approved, shall be performed through the service “My statements and payments” of SUNAT Virtual.

The corresponding payment can be made through the SUNAT service “My statements and payments”; of the Easy Payment System; in banks enabled using the SUNAT Payment Number (NPS); or, in cash or check in the banking network authorized by SUNAT.

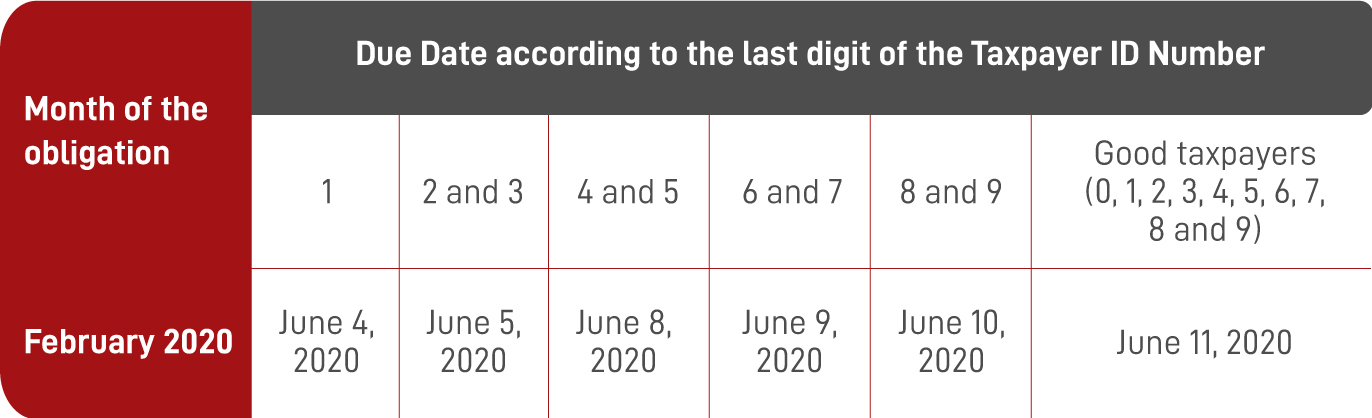

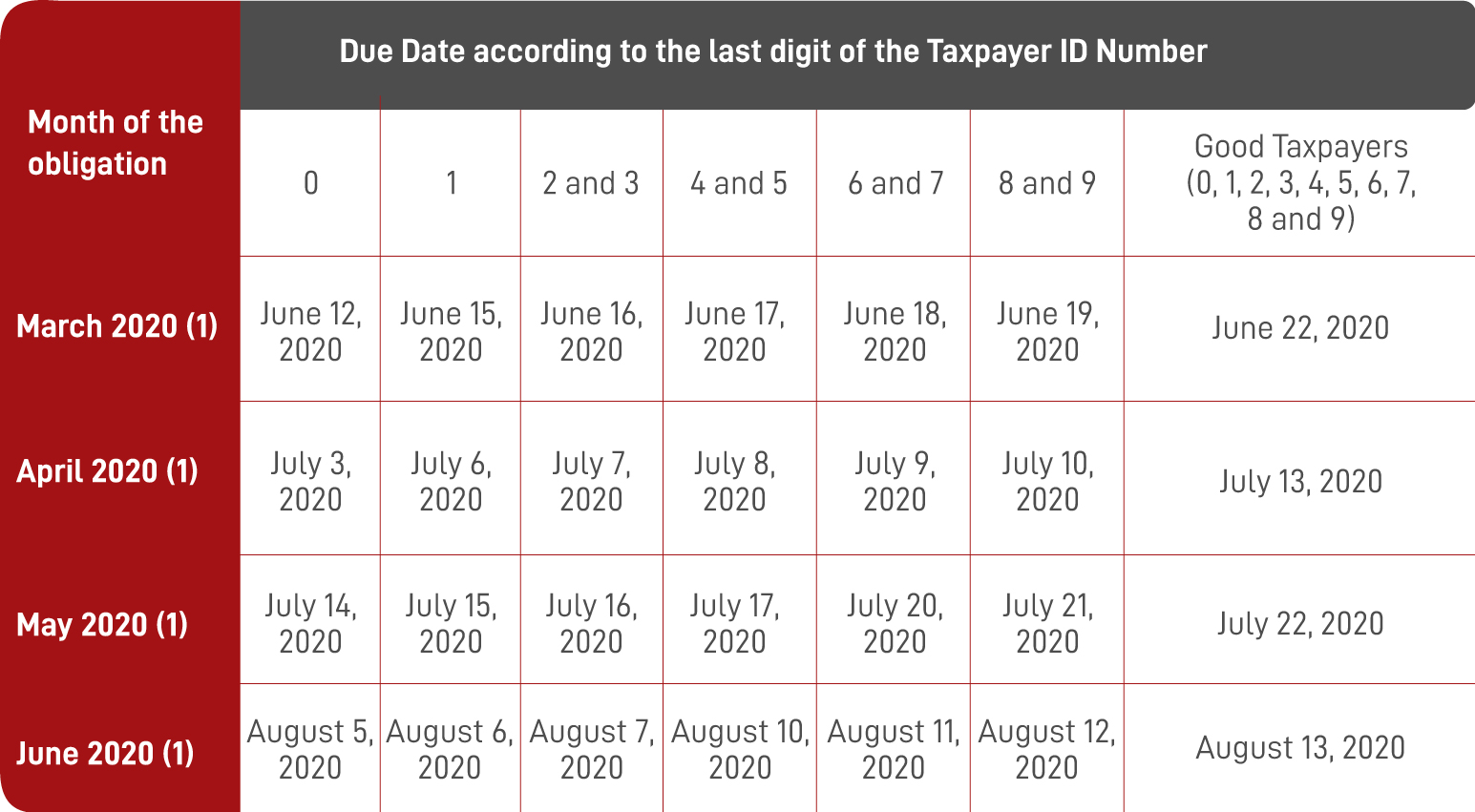

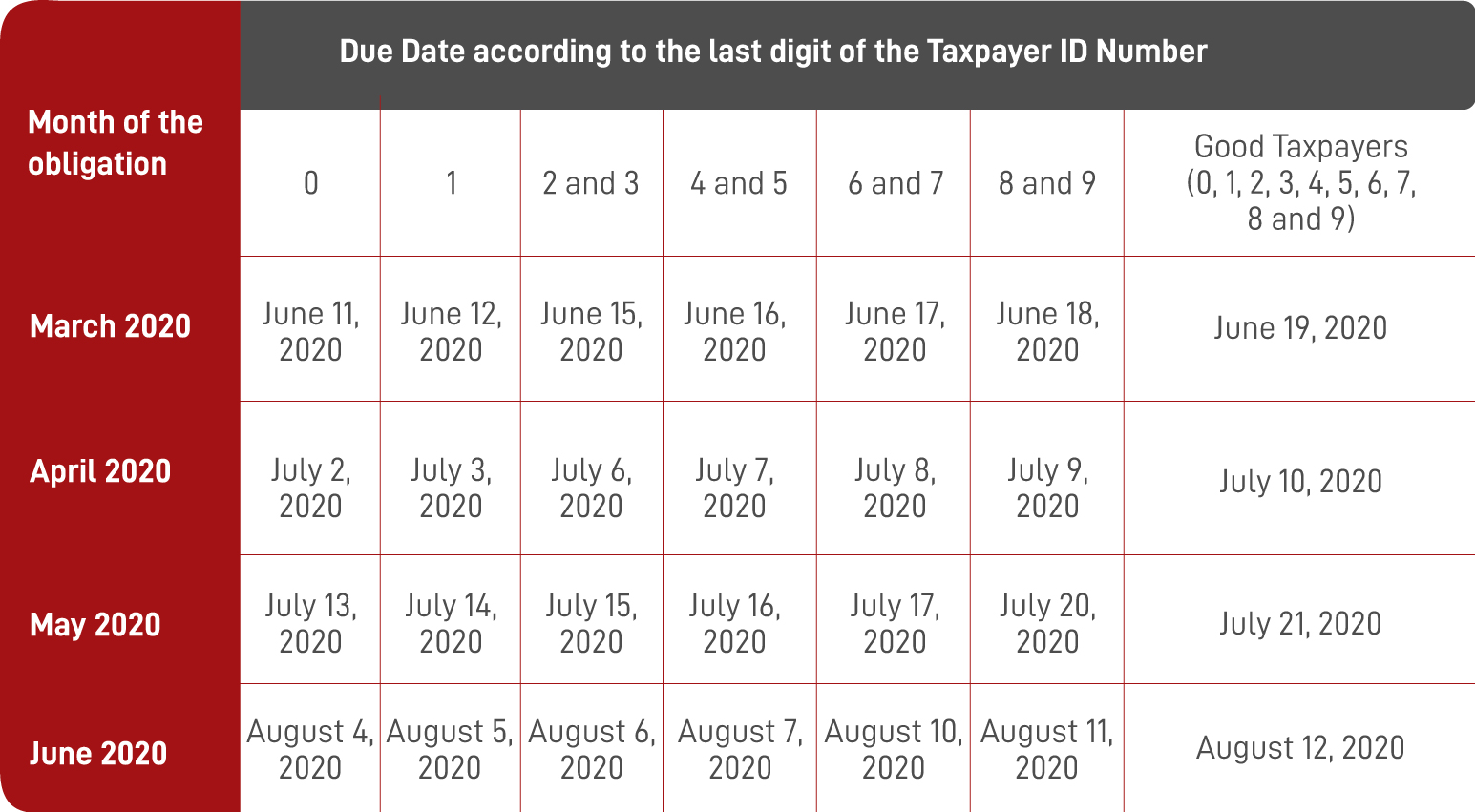

A new extension of the deadlines for the fulfillment of tax obligations is provided for by the extension of the national emergency declaration.- Due to the extension of the State of National Emergency until May 10, 2020, through Superintendence Resolution No. 075 -2020/SUNAT, published on April 29, 2020, new expiration dates for certain tax obligations are established:

A) For taxpayers receiving income from the third category who, in the taxable year, 2019 had earned net income of up to 2,300 UIT (S/.9,660,000.00) or who had earned or received income other than the third category which together do not exceed said amount:

i) The due dates for the statement and payment of the monthly tax obligations for the month of February 2020, including those related to the PLAME, are extended as follows:

B) For taxpayers receiving income from the third category who, in the taxable year 2019, had earned net income of up to 5,000 UIT (S/.21,000,000.00) or who had earned or received income other than the third category which together do not exceed said amount: i. i) The due dates for the statement and payment of the monthly tax obligations for the months of March to June 2020, are extended as follows:

ii) The maximum dates of delay of the Sales and Income Register and the Electronic Purchase Register of Annex III of the Superintendence Resolution No. 269-2019/SUNAT are extended (applicable to taxpayers obliged to keep books electronically from the 2020) from March to June 2020, as follows:

iii) Until May 25, 2020, the deadlines for submitting to SUNAT- directly or through the OSE, as appropriate- the informative statements and communications of the Electronic Emission System that originally expired from March 16, 2020 to May 10, 2020.

iiv) Until May 29, 2020, the deadline for submitting the DAOT for which the fixed deadline for submission would have been from March 16, 2020 to May 10, 2020.

Suspension or reduction of payments on account.- Legislative Decree No. 1471, in force from April 30, 2020, establishes a special regime to reduce or suspend payments on account of Income Tax from the months of April to July 2020. All taxpayers are eligible for the scheme, without exception, regardless of the method of calculation applicable to payments on account (coefficients or percentages). The rule is also applicable to taxpayers subject to special systems of payments on account of Income Tax. The suspension or reduction of payments on account from April to July shall be automatic without requiring the approval of SUNAT (which does not exempt the submission of the monthly statement of the respective advance).

Compensation of Balance in Favor.- In accordance with the precedent of mandatory observance contained in Resolution of the Tax Court No. 08679-3-2019, taxpayers have the right to request compensation of the balance in favor of Income Tax with different debts to payments on account of said tax. In order to enable this option, SUNAT has posted in the “Other Procedures and Procedures – Companies” section of its website the “Suggested Format to request compensation for the Balance in Favor of the 3rd Income Tax. Category- RTF No. 08679-3-2019”. (download here). Taxpayers who wish to request the aforementioned compensation must send an email to portalsunat@sunat.gob.pe, attaching the Form enabled by SUNAT (completed and signed by the legal representative) and a request in which the R.U.C. of the taxpayer and the data of the legal representative who signs the documents.

Judgment of the Constitutional Court: Selective Consumption Tax (ISC) applicable to casinos and slot machines.- Through the Judgment issued in file No. 00001-2019-PI/TC, the Constitutional Court rules on the constitutionality of the Decree Legislative No. 1419 amending the IGV and ISC Act, in order to incorporate casino games and slot machines within the scope of the ISC. In the unconstitutionality claim, it was alleged that the Legislative Decree does not regulate a tax that levies the consumption of users of casino games and slot machines, but, in fact, creates a tax on the profits and losses of the casino operator and slot machines; and that, in addition, the rule did not include online gambling, with unjustified unequal treatment. In this regard, the rapporteur proposed to declare the claim founded, however, this ruling did not reach the five votes necessary to declare the case unconstitutional. Consequently, the constitutionality of Legislative Decree No. 1419 is confirmed.

Christmas consumption vouchers for workers (RTF No. 8266-2-2019).- In this resolution, the Tax Court indicates that the expenses for the purchase of consumption vouchers for workers do not comply with the Causality Principle when the vouchers are not issued to workers. For this purpose, they must present, among other documents, a list with the name, ID number and signature of the workers who received vouchers.