INDECOPI APPROVED THE THRESHOLD CALCULATION GUIDELINES AND THE NOTIFICATION FORMS DERIVED FROM THE MERGER CONTROL LAW

On June 1, 2021, within the framework of the provisions of Law No. 31112, «Merger Control Law”, by means of the Resolution No. 022-2021/CLC-INDECOPI, the National Institute for the Defense of Competition and Protection of Intellectual Property – INDECOPI, approved the «Threshold Calculation Guidelines» («Guidelines«). Its purpose is to specify the elements that must be considered by economic agents and the authority in order to calculate the notification thresholds.

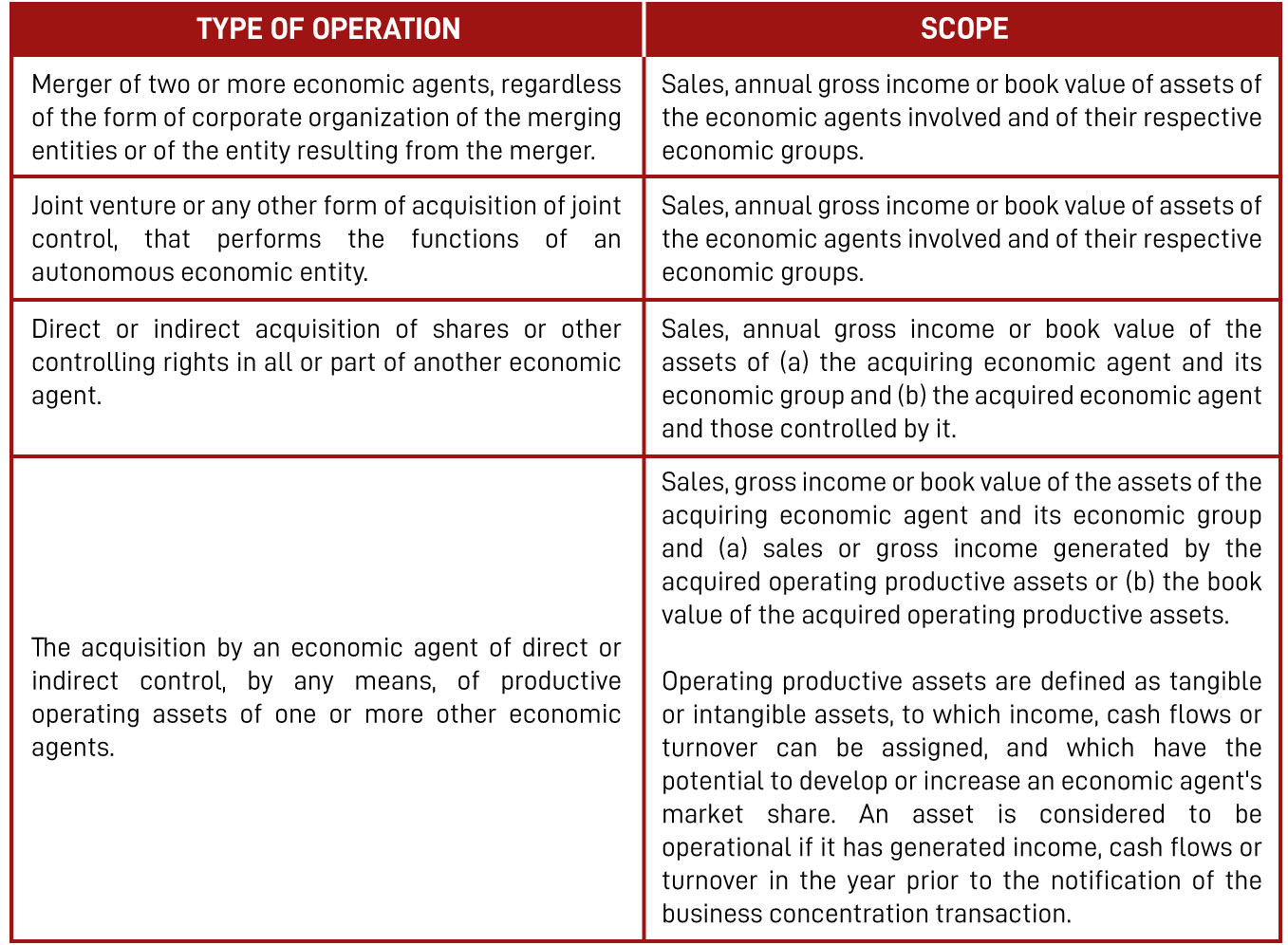

In this regard, the Guidelines specify and develop, among others, the following concepts:

It is also specified that, in the case of successive transactions, these must be notified if «(i) the income or sales of the economic agents in all successive transactions reach the joint and individual threshold; or, (ii) the value of the assets of the economic agents in all successive transactions reach the joint and individual threshold«.

3. Parameters for the calculation of the thresholds: As said before, the thresholds are calculated considering «gross sales or income», or «value of assets». According to the Guidelines establish, as the Merger Control Law does not link such concepts to any specific definition, the Guidelines may establish their own definitions according to the particular purpose of the notification thresholds. The abovementioned terms are defined as follows:

(i) Gross sales or income: The Guidelines state that «it is appropriate to establish as a general rule that the concept of «gross sales or income» includes all income or sales related to the normal line of business» that are made or generated in the country, understood as «all those activities that the economic agent performs on an ordinary basis to generate income». Likewise, it is specified that returns, offers, discounts, taxes, among others, will be excluded from the calculation of sales or income. Likewise, it is specified that only sales and income made or obtained in Peru should be included in the calculation.

(ii)Value of Assets: The Guidelines state that this amount will be obtained by considering the book value of the tangible and intangible assets located in the country. Regarding the latter, assets located in the country will be considered as those located in Peru and recorded in the financial statements of an economic agent incorporated in Peru. In the case of economic agents not incorporated in Peru, the following assets will be considered: (i) tangible assets located in Peru; (ii) intangible assets registered in any Peruvian registry (including INDECOPI’s registry of distinctive signs): and (iii) intangible assets derived from agreements entered into with economic agents incorporated in Peru.

Additionally, in the case of: (i) provision of services; (ii) international transportation; (iii) sales of tour packages; and (iv) internet sales, specific localization rules outlined in the Guidelines must be followed.

Likewise, the Ordinary Notification Form and the Simplified Form were published. These contain the requirements to submit the request for authorization to carry out a business concentration transaction before INDECOPI. Both forms are available at the following links: (i) Ordinary Notification Form: https://bit.ly/3oYuXpo and (ii) Simplified Notification Form: https://bit.ly/3i2EVV9

The Guidelines are available at the following URL: https://bit.ly/3fQJHCJ

For further information, please contact Verónica Sattler (vsattler@estudiorodrigo.com) and/or Ítalo Carrano (icarrano@estudiorodrigo.com)