Ministerial Resolution No. 134-2020-EF/15 was published on April 13, 2020. This Resolution approves the Operating Regulations (the “Regulations”) of the REACTIVA PERU Program to Ensure Continuity in the Chain of Payments in response to the Impact of COVID-19 (the “Program”), approved by Legislative Decree No. 1455, amended by Legislative Decree No. 1457 (the “Decree”), and through which a program of regulated guarantees for credits granted by financial institutions was created for up to S/.30,000 million.

As previously reported, the Regulation was pending in order to regulate several relevant matters. In accordance with the Regulations and in addition to the provisions of the Decree, the main features of the Program are described below:

1. This is a credit guarantee program and not a line of credit or a direct financing fund. Loans are granted by financial institutions which receive operating funds from the Central Reserve Bank of Peru (BCRP). The total guarantee of the program is for up to S/. 30,000 million soles.

Loans included under this system will be granted from the date of issue of the Regulation (April 13, 2020) until June 30, 2020.

2. The guarantee for each credit is up to the amount equivalent to (i) the contribution to EsSalud of 2019 or (ii) one month of average monthly sales in 2019, according to the information that has been reported to SUNAT. In the case of micro-sized enterprises, only the sales criteria shall be used. Microenterprises are defined as those with annual sales up to 150 Tax Units (S/.645 thousand).

In no case the amount to be lent to a debtor will exceed S/.10 million soles, in addition to the interest derived from its use in BCRP operations.

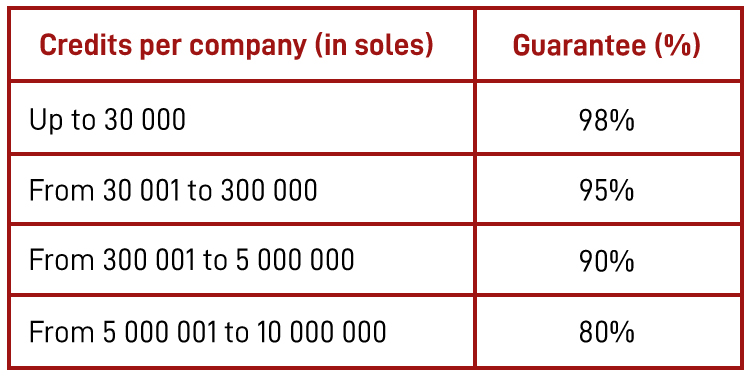

3. The guarantee covers the absolute balance of credits disbursed by participating financial institutions, between 80% and up to 98%, depending on the amount disbursed by the debtor, as detailed below:

4. The Regulation has not limits regarding the interest rate, but merely stated that the applicable rate reflects the cost of funding (which should be the cost of the transaction with the BCRP) and the margin of the financial institution, although it does indicate that the rate must comply with the conditions of the operations as established by the BCRP.

Also, to the extent that there is a tranche of credit that would not be guaranteed, that portion could have an impact on the margin and, therefore, on the final interest rate to be allocated to said loans.

5. The Regulation extends the restrictions on the use of funds included in the Decree, mainly related to the obligation for loans under the Program to be new credits (not refinancing). Thus, the companies benefiting from these credits will not be able to prepay financial obligations other than the credits granted under the Program, as long as these remain in force.

To sum up, with inclusions, loan funds can NOT be used to:

a) pay or prepay financial obligations due or pay overdue obligations to the financial institution;

b) acquire fixed assets;

c) purchase shares in companies, bonds and other monetary assets;

d) make capital contributions;

6. Regarding eligibility for the Program, certain criteria are clarified and an “Exclusion List” of activities or products is included, so that individuals or companies must comply with the following in order to be part of the Program:

a) Not have tax debts managed by SUNAT, enforceable in coercive collection greater than one (01) Tax Unit as of February 29, 2020, corresponding to tax periods prior to 2020.

b) If classified at the SBS Risk Center as of February 2020, at least 90% or more of its credit operations in the financial system are rated “Normal” or “With Potential Problems” (CPP).

If not classified by that date, you must have been in a “Normal” category considering the 12 months prior to the granting of the loan. Be advised that those that do not have a classification in the SBS may also apply within the 12 months prior to the granting of the loan.

c) Not be linked to the financial institution providing the loan.

d) Not fall within the scope of Law No. 30737 (Law that ensures the immediate payment of civil reparation in favor of the Peruvian State in cases of corruption and related crimes).

e) Not engaging in, or intending to develop, the activities or manufacture of products listed in the “Exclusion List” set out in Annex 1 of the Regulations. These include activities involving forms of forced labor or exploitation, businesses of negative social perception (prostitution, manufacture or trafficking of weapons, tobacco production, narcotics or alcoholic beverages (other than wine, beer and pisco), casinos, radioactive materials (except for medical equipment or equipment with minimal or protected radioactive sources), substances subject to global phase-out, production, trade, storage or transportation of relevant volumes of dangerous chemicals, illegal mining, wood or other forest products (without authorizations and management plan), those that may damage lands of indigenous peoples or vulnerable groups or that may adversely affect archaeological sites or sites of cultural importance, among others.

This requirement is fulfilled with the presentation of an affidavit from the debtor company whose falsity results in the acceleration of the loans, as well as the execution of any guarantee. The financial institution cannot grant waivers in this regard.

7. Debtor companies must not distribute dividends or approve the distribution of profits during the term of the loan, except for the amount of participation in workers’ profits.

Likewise, the debtor companies will allow COFIDE and the financial institution access to their tax information.

8. The maximum term is 36 months to pay which includes a grace period (of capital and interest) of up to 12 months. Interest corresponding to the grace period is prorated during the remaining term of the loan, which is paid in equal monthly installments once the grace period has ended. The debtor company may request the reduction of payment terms once the credit has been granted, which is reported to COFIDE and the BCRP.

9. The guarantee may be given in two ways, (i) as a guarantee to the credit portfolios of a financial institution, through a title trust (to be managed by COFIDE) that pays the entities the unpaid amount of their portfolio at the end of the Program term; or (ii) in favor of the financial institution, by means of an individual guarantee to the security that represents the debt (for loans above S/.10,000).

The guarantee is approved by Supreme Decree with the approval of the Council of Ministers, countersigned by the President of the Council of Ministers and the Minister of Economy and Finance. For this, a prior report from the Office of the Comptroller General of the Republic will be required to be issued in no more than four (4) working days after the request is submitted by the Ministry of Economy and Finance.

10. The program will be managed by COFIDE, institution that will be responsible, among other tasks, for verifying that the credits of the program meet the requirements and conditions for the guarantee, as well as for following collection processes if required.

11. The guarantee is honored after 90 consecutive days of arrears. The credits that are honored through the guarantee of the Program are transferred to a trust for collection. In other words, in the event that the 90 days elapse without the debt having been paid and once the financial institution have exhausted the collection methods, it can use the guarantee, collect the unpaid balance and then the trust managed by COFIDE assumes the credit balance and may make the collection.

The guarantee is effective since COFIDE issues the corresponding certificate and expires if COFIDE detects that there are loans that do not meet the criteria of the Program and inform the BCR. The financial institution may replace the credit observed by another that meets the conditions.

12. The financial institution has the power to decide what type of collection to carry out for the recovery of the loan in accordance with the applicable regulation and its internal policies or processes, and may even determine the advisability of punishing any loan which must be reported to COFIDE stating that said decision has been taken in accordance with said applicable laws and internal policies or processes.

We will extend the above in the event that modifying or complementary regulations are published regarding the Program. Meanwhile, we remain at your disposal to answer any questions about this Program.