The Legislative Decree No. 1455, published on Monday April 6, 2020, creates the REACTIVA PERU Program to Ensure the Continuity of the Payment Chain in response to the Impact of COVID-19 (the “Program“), through which a program of state guarantees is created for credits that are granted by financial institutions for an amount of up to S/ 30,000 million.

Although the issue of the Operational Regulations is still pending (which shall regulate in detail several relevant matters, and which should be published within five business days), below are the highlights of the Program:

1. It is a credit guarantee program, not a credit line or a direct financing fund. Loans are granted by financial institutions, which receive funds from the Central Reserve Bank of Peru (BCRP). The total guarantee of the program is for up to S/ 30,000 million soles.

Credits under this system will be granted from the moment the Operational Regulations are issued until June 30, 2020.

2. The guarantee for each credit is for up to the smallest amount between (i) three (3) times the annual contribution to Essalud(social security)in 2019 and (ii) one month of average monthly sales in 2019, according to the information reported to SUNAT. In the case of micro-sized enterprises, the sales criterion shall only be used.

In no case the amount to be lent to a debtor will exceed S/ 10 million soles. Although the following issue is not established in the Legislative Decree (and it would be necessary to consider whether the Operational Regulations will regulate this matter or not), when establishing a limit per debtor and not per credit, it could be understood that more than one credit can be requested to different financial institutions, provided that such threshold is not exceeded (and the maximum amount per company).

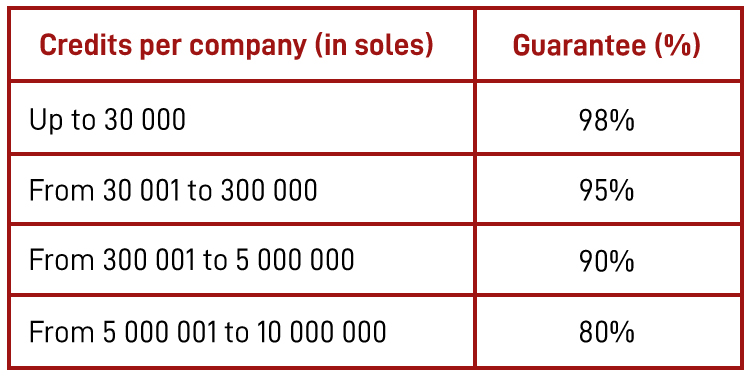

3. The program guarantees the loans granted by the participating financial institutions, from 80% and up to 98%, depending on the amount disbursed to each debtor, as detailed below:

The higher the amount, the lower the guarantee coverage and, greater the exposure of the financial institution. This should lead banks to do carry out a credit analysis for the approval of the loan (which will be higher or lower depending on the amount and percentage of risk they take).

Furthermore, as there is a tranche of the loan without the government’s guarantee, such could have an impact on the Operational Regulations will establish the criteria for determining the interest rate applicable to Program’s credits.interest rate to be applied to the loans. Possibly some rules will apply to this determination, since the Legislative Decree states that the

4. Loans under the Program must be new credits, and cannot beused to refinanceexisting obligations and, therefore, the companies benefiting from these credits will not be able to prepay financial obligations other than the credits granted under the program, as long as these remain in force.

5. With regard to the beneficiary companies:

a. They should not owe SUNAT more than 1 Tax Unit (S/ 4,300) in owed taxes under coercive collection, as of February 29, 2020;

b. Their risk rating asofthe date above must be “Normal” or “With Potential Problems”;

c. They may not be related to financial institutions;

d. They may not be included in Law No. 30737 (Law that ensures the immediate payment of civil remedy to the Peruvian State in the cases of corruption and related offences);

e. They must not distribute dividends or profits (except dividends or profits for workers) during the term of the credit;

f. They will allow access to their tax information and sworn statements required for the verification of the credits (the verification methodology will be included in theOperational Regulations);

The Operational Regulations may establish additional criteria.

6. The maximum term of payment is 36 months, which includes a grace period (principal and interest) of up to 12 months.

7. The guarantee can be given in two ways: (i) as a guarantee to the credit portfolios of a financial institution, through a trust (to be administered by COFIDE) that pays the entities theunpaidamount of their portfolio at the expiry of the Program term; or (ii) in favor of the financial institution, by means of an individual guarantee to the security representing the debt.

8. The program will be managed by COFIDE, institution that will be responsible, among other tasks, for verifying that the program credits meet the requirements and conditions for the guarantee, as well as for following collection processes if required.

9. The guarantee is honored after 90 days ofdefault. Credits that are honored through the Program guarantee are transferred to a trust for collection. In other words, in the event that the 90 days elapse without the debt having been paid and once the financial institution have exhaustedall collection methods, it can use the guarantee, collect the unpaid balance and then the trust managed by COFIDE assumes the credit balance and may seek the collection.

The information above will be complemented once the Operational Regulations are published. In the meantime, we remain at your disposal to answer any questions you may have about this Program.