I. Amendments related to Income Tax

– Income tax exemptions were extended.- Law No. 31106, published on December 31, 2020, extends the validity of the exemptions contained in Article 19 of the Income Tax Act (LIR) until December 31, 2023.

– Reference to the limit for the deduction of interest expenses was specified in the year 2021.-

The Third Final Complementary Provision of Supreme Decree No. 432-2020-EF specifies that in order to deduct interest as an expense (paragraph a) of Article 37 of the LIR), taxpayers who are incorporated or start activities in the year 2021 shall consider the EBITDA of such year.

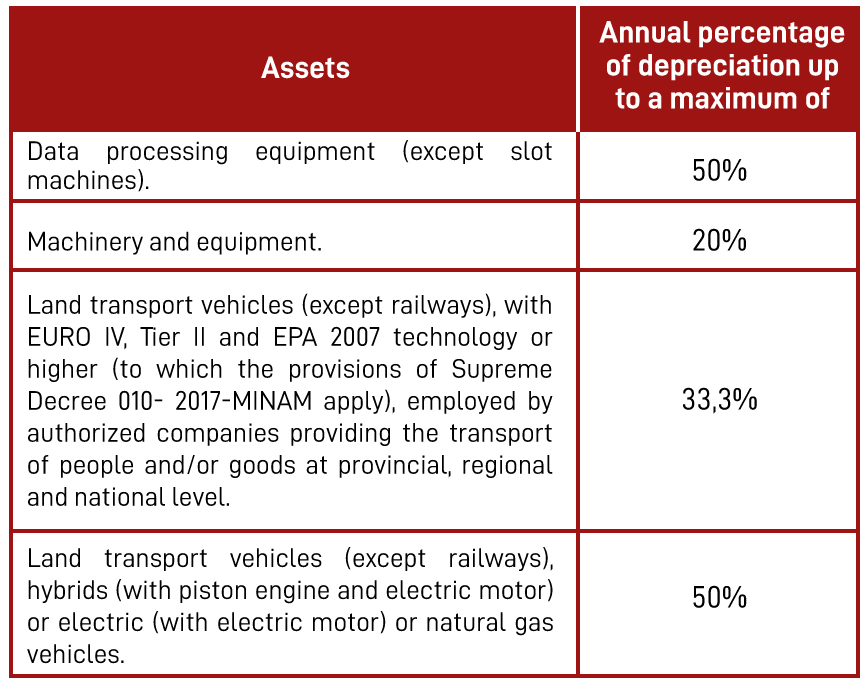

– Amendment of the special depreciation regime provided for by Legislative Decree No. 1488.- Law No. 31107, published on December 31, 2020, amends Legislative Decree No. 1488 as follows

i) From fiscal year 2021, the following percentages shall be applied:

ii) The depreciation of buildings and constructions applying 20% per annum shall be carried out until total depreciation or only during fiscal years 2021 and 2022. The choice is made by the taxpayer when he submits his annual income tax return; and it is immovable.

– Amendments to the Income Tax Act (LIR).- Law No. 31108, published on December 31, 2020, Article 65 of the LIR was amended to establish that domiciled individuals who obtain exclusively third-category income or losses generated by investment funds, trust assets of securitization companies and/or bank trusts are not required to keep accounting books and records.

– Amendments to the Income Tax Act (LIR).- Supreme Decree No. 425-2020-EF, published on December 31, 2020, amends Article 39-A to indicate that the withholding of tax is not applicable when the companies that manage mutual investment funds pay income by crediting the bank accounts that the distributors of participation shares, acting on behalf of the participants of such funds, dispose thereof.

– Additional deduction of fourth and fifth income category.- Supreme Decree No. 432-2020-EF, published on December 31, 2020, establishes the following limits and conditions for the additional deduction of expenses referred to in paragraph d) of Article 26-A of the Regulations of the Income Tax Act:

i) 50% of the amounts paid for tour guide services, adventure tourism services, ecotourism and artisan services supported by receipts for fees are deductible.

ii) 25% of the amounts paid for travel and tourism agency services and artisan activities supported by receipts (invoice, sales slip) are deductible.

II. Amendments related to tax benefits

– The tax benefits of the Agrarian Regime are repealed.- Law No. 31087, published on December 6, 2020, repealed Law No. 27360, Act for the Promotion of the Agrarian Sector, which, among other tax benefits, established a 15% income tax rate for the third category and accelerated depreciation at an annual rate of 20% of the amount of investments in hydraulic infrastructure and irrigation works.

The following arrangements shall apply from January 1, 2021.

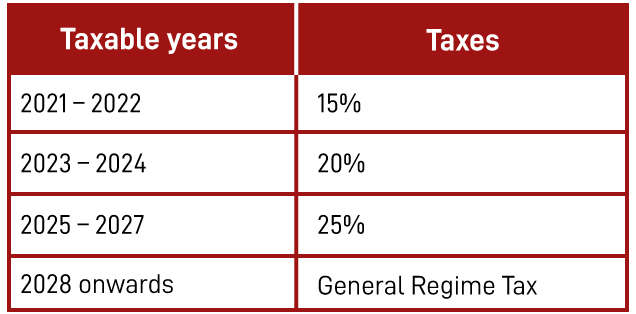

– New tax regime for the agricultural sector. – Article 10 of Law No. 31110, published on December 31, 2020, establishes the following tax benefits for natural or legal persons that develop crops and/or breeding (with the exception of agro-industrial activities related to wheat, tobacco, oil seeds, oils and beer):

I. Income Tax shall be determined by applying the following rates to net income:

i) For individuals or legal entities whose net income does not exceed 1,700 (one thousand seven hundred) UIT in the taxable year:

ii) For individuals or legal entities whose net income exceeds 1,700 (one thousand seven hundred) UIT in the taxable year:

ii) The amount of investments in hydraulic infrastructure and irrigation works may be depreciated at a rate of 20% per year. Benefit applicable until December 31, 2025.

iii) The use of the Special Regime for Early Recovery of the General Sales Tax adopted by Legislative Decree No. 973. Benefit applicable until December 31, 2025.

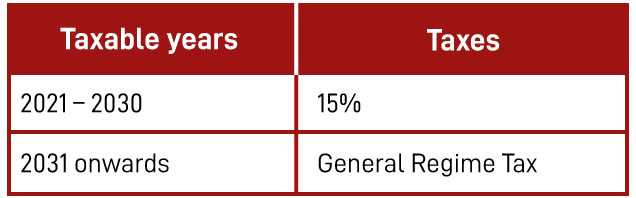

iv) Individuals whose net income does not exceed 1,700 UIT in the taxable year shall be entitled to a tax credit of 10% of the reinvestment of up to 70% of the amount of annual profits, after payment of income tax, during the period from 2021 to 2030.

– Benefits and exemptions are extended.- Law No. 31105, published on December 31, 2020, extends the term of the tax credit until December 31, 2021:

i) Tax refunds on purchases by foreign donations and imports from diplomatic missions.

ii) Exemption from the IGV for the issuance of electronic money by companies issuing electronic money.

iii) Exemptions contained in Appendices I and II of the GST Act

– The Deferral and/or Fractionation Regime for the Tourism Sector (RAF-TURISMO) was adopted. – Law No. 31103, published on December 31, 2020, establishes the RAF-TURISMO with respect to tax debts administered by SUNAT that constitute revenue from the Public Treasury or ESSALUD, in order to mitigate the impact on said sector of the declaration of a state of national emergency as a result of COVID-19.

Tourism service providers and/or artisans whose annual net income for the taxable year 2019 does not exceed 2,300 UIT’s (S/ 9,660,000.00) may benefit from this regime.

– Refund of the Temporary Net Assets Tax (ITAN) for the year 2020.- Law No. 31104, published on December 31, 2020, provides, exceptionally, for the refund of the ITAN for the year 2020 within a period not exceeding thirty (30) working days by means of a credit to the account. Upon expiration of such term, the applicant may consider its application approved.

III. Formal obligations to SUNAT

– Value of the Tax Unit (UIT) for 2021 was amendment.-Amendment of the special depreciation regime provided for Supreme Decree No. 392-2020-EF, published on December 15, 2020, sets the value of the Tax Unit (UIT) for 2021 at S/. 4,400 (four thousand four hundred soles).

– Provisions for the Income Tax Return for the Taxable Year 2020.- Through Superintendence Resolution No. 229-2020/SUNAT, published on December 30, 2020, Resolution No. 271-2019/SUNAT was amended as follows:

i) Taxpayers who generate third-category income may also use the SUNAT People APA to file their annual income tax return.

ii) The virtual forms for the 2020 tax return shall be available in accordance with the following:

(iii) The following schedule for the submission of the declaration is adopted:

– Schedule for compliance with tax obligations was adopted in 2021.-

Superintendence Resolution No. 224-2020/SUNAT, published on December 27, 2020, establishes the schedules for compliance with various monthly obligations before SUNAT and the maximum dates of delay of the Electronic Sales and Income and Purchase Registries for the year 2021.

– Deadline for the authorization of printing, importing or generation of documents in contingency was extended.- Through Resolution No. 221-2020/SUNAT, published on December 27, 2020, the term is extended until December 31, 2021 for the authorization of printing, importing or generation of documents in contingency by means of computerized systems.

– The Regulations governing the provision of financial information to SUNAT to combat tax evasion and avoidance was adopted.- Supreme Decree No. 430-2020-EF adopts the following regulatory provisions:

i) Companies in the financial system must provide SUNAT with the identification data of the holder or registered holder and the account data when there are amounts in excess of S/ 10,000 (ten thousand soles).

ii) Financial information shall be provided to SUNAT on a monthly basis.

Deduction of expenses for donations.- Report No. 123-2020-SUNAT/7T0000 states that for the deduction regulated in paragraph x) of Article 37 of the Income Tax Act, it is not a condition that the destination of the donated goods be proved.

Special depreciation regime.- Report No.115-2020-SUNAT/7T0000 establishes that vessels and ships are not included in the term «buildings and constructions» referred to in Article 3 of Legislative Decree No. 1488, which established a special depreciation regime.

Transfer on the occasion of the winding-up of an association.- Report No. 119-2020 SUNAT/7T0000 concludes that the transfer of assets and liabilities by a non-profit association, on the occasion of its liquidation, in favor of a similar association of which it was a member, is not taxed with the IGV.

Statement of the Final Beneficiary.- Report No. 111-2020-SUNAT/7T0000 establishes that:

i) Public law companies created by law, whose sole shareholder is the Peruvian State, are exempted from submitting Virtual Form No. 3800 – Statement of the Final Beneficiary.

ii) If the public law companies created by law are shareholders, in turn, of a corporation incorporated and domiciled in the country, the statement of the final beneficiary of such corporation must consider the information on the final beneficiary of the public law companies that are its shareholders.

Validity of the notification of requirement of Article 75 of the Tax Code (RTF No. 6741-4-2020).- Through this resolution, the Tax Court establishes the following criterion of mandatory compliance:

«The notification of the injunction issued under the second paragraph of Article 75 of the Tax Code, when the audit period provided for in Article 62-A of said code has expired, is in accordance with the law, as long as the conclusions of the audit procedure are communicated with said injunction and no additional information and/or documentation is requested.

Technical Support Service Support (RTF No. 11756-1-2019).- SUNAT questioned the tax credit for the technical support service in one of the technological headquarters of the taxpayer for not having accredited the causality of the transaction.

The taxpayer delivered the invoices, the accounting entry, the purchase order with the description of the service, a document called payment to third parties, the bank statement showing the charge for the payment of the transaction, and e-mails of internal communication among the personnel; however, both SUNAT and the Tax Court considered that these documents were insufficient; and it was pointed out that reports of the technical personnel who performed the support work and the conformity of the work or service should have been submitted.

Entry into force of the Agreement to Avoid Double Taxation (CDI) between Peru and Japan.- Through Legislative Resolution No. 31098, published on December 29, 2020, the Agreement between the Republic of Peru and Japan to avoid double taxation in relation to income taxes and to prevent tax evasion and avoidance and its Protocol, signed on November 18, 2019, was adopted.

Subsequently, on December 30, 2020, Supreme Decree No. 060-2020-RE was published, which ratified the aforementioned Convention. Thus, the CDI Peru-Japan is in force since January 1, 2021.