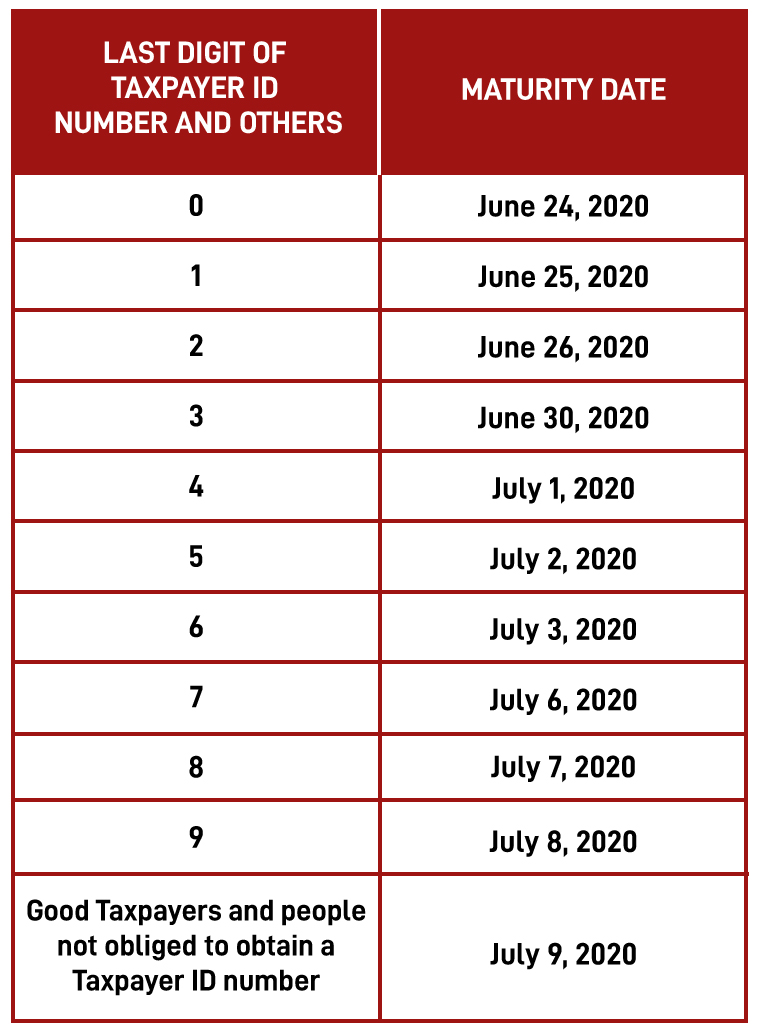

The Annual Income Tax Return Schedule is modified.- Through Superintendency Resolution No. 054-2020/SUNAT, the maturity schedule of the Annual Income Tax Return and the Financial Transaction Tax has been modified for tax debtors receiving third category income, who in taxable year 2019 would have earned a net income of up to 2,300 Tax Units (S/ 9’660,000.00) or who would have obtained or received income other than third category, which added up do not exceed the amount above. The new deadlines are the following:

Therefore, the original maturity schedules for the annual payment and tax return of all other taxpayers not included in this resolution are maintained to date (Seventh Supplementary Final Provision of Superintendency Resolution No. 271-2019/SUNAT).

Deadlines for the fulfillment of tax obligations are extended due to the declaration of national emergency.- Through Superintendency Resolution No. 055-2020/SUNAT, the following measures have been established after the declaration of national emergency as a result of Coronavirus (COVID-19) for taxpayers receiving third category income, who in taxable year 2019 would have earned a net income of up to 2,300 Tax Units (S/ 9’660,000.00) or who would have obtained or received income other than third category, which added up do not exceed the amount above:

i. The due dates for the tax return and payment of monthly tax obligations for the month of February 2020 are extended as follows:

| Month of the obligation | Due Date according to the last digit of the Taxpayer ID Number | |||

| 1 and 2 | 3, 4 and 5 | 6, 7, 8 and 9 | Good taxpayers

(0, 1, 2, 3, 4, 5, 6, 7, 8 and 9) |

|

| February 2020 | April 3, 2020 | April 6, 2020 | April 7, 2020 | April 8, 2020 |

ii. The maximum dates of delay of the Register of Sales and Revenues and the Register of Electronic Purchases of Annex II of Superintendency Resolution No. 269-2019/SUNAT for the month of February 2020 are extended, as follows:

| Month of the obligation | Due Date according to the last digit of the Taxpayer ID Number | |||

| 2 | 3, 4 and 5 | 6, 7, 8 and 9 | Good taxpayers

(0, 1, 2, 3, 4, 5, 6, 7, 8 and 9) |

|

| February 2020 | April 2, 2020 | April 3, 2020 | April 6, 2020 | April 7, 2020 |

iii. The maximum deadline with respect to tax related books and records that are kept physically (Resolution No. 234-2006/SUNAT) and electronically (Resolution No. 286-2009/SUNAT) -which originally expired between March 16, 2020 and March 31, 2020- were extended until April 1, 2020.

iv. The delivery deadlines for submission to SUNAT, directly or through OSE where applicable, of information statements and communications from the Electronic Issuing System, -which originally expired from March 6, 2020 until March 31, 2020- were extended until April 15, 2020.

v. The deadline for submitting the Annual Declaration of Transactions with Third Parties (DAOT),-which originally expired from March 16, 2020 to March 31, 2020- were extended until April 7, 2020.

vi. It is provided that these new due dates will be applied in order to account for the period that taxpayers have to submit a request for the refund of credit balance in connection with the profit from March or later months.

Therefore, the original maturity schedules for the annual tax return and payment of all other taxpayers not included in this provision are maintained to date.

Real Estate Investment Funds (FIRBI): Information regarding the final income tax withholding.- Emergency Decree No. 009-2019 established that the provisions related to the information published by SUNAT regarding the application of income tax incentives that are regulated by Legislative Decree No. 1188, would be now regulated by a Supreme Decree.

Supreme Decree No. 025-2020-EF establishes that the information related to the final Income Tax withholding applicable to rental income or other onerous form of assignment in use of immovable property corresponding to taxable years 2020, 2021 and 2022 will be published in the SUNAT Transparency Portal until the last business day of July 2021, 2022 and 2023 respectively. It is also established that, for the purposes of the publication, natural persons are considered to the natural persons themselves, undivided estates and marital partnerships that chose to pay taxes as such, domiciled in the country.

Tax treatment of Badwill.- According to Report No. 193-2019-SUNAT/7T0000, the accounting recognition of the negative goodwill called Badwill does not generate income taxed with the Income Tax.

Report No 302-2003-SUNAT/2B0000, which established that the income earned as a result of the Badwill was subject to the tax, is rendered ineffective.

Additional fee applicable to branches. – Report No. 018-2020-SUNAT/7T0000 establishes that the additional 5% rate on the sums referred to in section g) of Article 24-A of the Income Tax Law (indirect disposal of income subject to subsequent tax control) does not apply to the branches of companies non-domiciled in the country, since the provisions of the second paragraph of section e) of Article 56 of such Law shall be considered in this scenario (5% lien on the disposable income in favor of the foreign holder).

Attributed third category income or loss.- Report No. 019-2020-SUNAT/7T0000 analyses the formal obligations related to third category income or losses attributed by fund or trust estate management companies or securitization firms, which do not qualify as FIRBIS or FIBRAS, in favor of natural persons during fiscal year 2019.

To this regard, the following was concluded:

i. Natural persons who receive third-category income as a result of the allocation of funds or trust are obliged to include the income or loss attributed by such fund or trust in their Income Tax Return.

ii. The natural person who receives the third-category income or loss from this type of investment fund or trust and who does not receive any other third-category income other than the income attributed by such fund or trust, is obliged to keep accounting books and records.

Final beneficiary of the Mutual Fund for Investment in Securities (FMIV).- Through Report No. 004-2020-SUNAT/7T0000, SUNAT establishes following conclusions regarding the determination of the final beneficiary of the FMIV referred to in Legislative Decree No. 1372:

i. The final beneficiary is any natural person who has the status of investor in an FMIV and who exercises final effective control of the estate, or who is entitled to the fund’s results or profits; without having to assess the amount of its participation in order to determine the rating of final beneficiary.

ii. The tax return of a final beneficiary of an FMIV shall include all the natural persons holding the status of investors at the relevant reporting date; whereas there is no provision to exclude any of them.

iii. If the investors in the FMIV are corporations or other legal entities, the latter shall be obliged to provide the data of their final beneficiaries, so that the assessment of the final beneficiary of an FMIV does not only include the natural persons who have the status of direct investors in that fund, but also those that have said status in the legal entities that are also investors in said FMIV.

iv. If during the same month, there are contributions and redemption of shares in an FMIV, with the consequent entry and exit of certain investors, there is an obligation to update and submit a new tax return from the final beneficiaries to SUNAT; this is an obligation that is not weakened by the number of shares of the redemption or contribution; or the percentage such transactions represent in the total assets of the FMIV.

v. If during same month there were only share redemptions without new investors joining the FMIV, the FMIV would be obliged to update the tax return, taken into account that by virtue of paragraph 9.2 above a change in the information provided by the final beneficiary regarding the participation rate has changed.

vi. If, during the same month, the same investor pays a contribution as well as a redemption, it is appropriate to update the tax return for the purpose of submitting the information related to the final beneficiary status of that person (for example, its inclusion and exclusion in the same period), despite the fact that it will no longer be an investor or shareholder at the end of the month.

Scope of the Vehicle Tax (RTF Mandatory Compliance No. 01865-7-2020).- The following mandatory compliance criterion is established:

“The 3-year-old period referred to in the tax relief scenario regulated in paragraph g) of article 37 of the Single Revised Text of the Municipal Tax Law, is counted from January 1 of the year following the year of manufacture of the vehicle”.

Loss of tax return benefit Selva Region Refund (Cassation No. 7758-2017).- In this judgment, the Standing Constitutional and Social Law Division of the Supreme Court confirms the position of the Tax Court and the Court of Appeals, and establishes that the lack of the stamp of the obligatory control point does not cause the loss of the tax return benefit Selva Region.

Such Division states that the purpose of the General Sales Tax Law, in order to have the Tax Refund benefit, is that the goods have been consumed in the Selva Region, which is not affected by formal observations. Also, it is unreasonable to give an essential or indispensable status to this stamp, especially in cases where the Tax Administration has carried out a physical inspection of the goods.

Broadcasting of programs via cable television (RTF No. 7306-2-2019).- Through this Resolution, the Tax Court states that the service by means of which a non-domiciled company grants an exclusive license to broadcast the audio and video signals in Peru of their programs through the cable television system in national territory qualifies as a use of services and, it is therefore taxed with the IGV, since the license allows the contractor to distribute and broadcast television channels or the programming of non-domiciled companies, that is, to economically exploit the broadcast programming of those companies in national territory, offering those services to its customers and local subscribers.

Nullity of values reported on the same day of the result of the supervision requirement (RTF No 6378-8-2019).- The Tax Court establishes that it is not valid to notify on the same day, the result of the supervision requirement and the resolutions of Final Determination and Assessment of Penalties, since the latter is the basis of the result; and since the result only takes effect on the working day following its notification, these resolutions were issued on the basis of an act which was not yet effective.

Final Determination and Assessment of Penalties are based on the assessments set out in the supervision results and, therefore be issued only from the date on which those findings became effective. It is for this reason that, pursuant to section 2 of article 109 of the Tax Code, it is appropriate to declare nullity when the results and values are notified on the same date.

Chile: Collection of VAT on services provided via digital platforms.- Law No. 21.210, which will enter into force on June 1, 2020, will tax the following services provided via digital platforms with the Value Added Tax (VAT)

i. The outsourcing of services rendered in Chile or sales made in Chile or abroad, provided that these sales give rise to an import.

ii. The delivery of digital entertainment content, such as videos, music, games or similar, through download, streaming or other technology, including texts, magazines, journals and books.

iii. The provision of software, storage, platforms or information technology infrastructure.

iv. Advertising, regardless of the medium or support through which it is delivered, materialized or executed.